S&P PUTS THE U.S. CREDIT RATING OUTLOOK TO NEGATIVE?

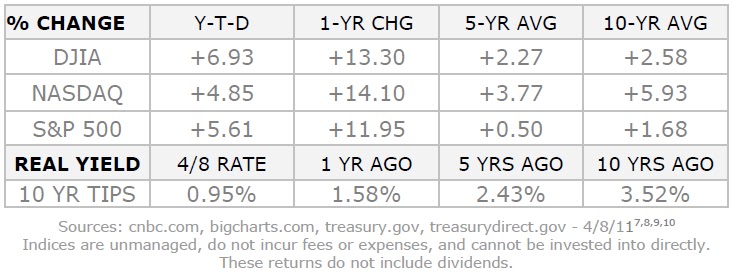

Standard & Poor’s rattled Wall Street early last week when it revised its outlook on U.S. long-term debt from “stable” to “negative”. I'm not sure if S&P was trying to make a statement of "we're on top of things" after they surely weren't in regards to the exotic mortgage instruments of years past. Regardless of the reason, their action was utterly foolish and absurd. Across the next three trading days, earnings sent the market higher. The four-day week turned into a winning one, as the numbers show: DJIA, +1.33% to 12,505.99; S&P 500, +1.34% to 1,337.38; NASDAQ, +2.01% to 2,820.16.5,6

HOME SALES, HOME STARTS IMPROVE IN MARCH

The National Association of Realtors announced that existing home sales were up 3.7% last month, about 1% higher than the rebound expected on Wall Street. (NAR noted that about 35% of these were cash sales.) In another positive development for the real estate market, the Commerce Department measured a 7.2% gain in housing starts and an 11.2% rise in construction permits for March.1

GOLD AT NEW HIGH, DOLLAR TOUCHES 3-YEAR LOW

Gold cracked the $1,500 ceiling last week. Prices reached $1,508.75 on Thursday before settling at $1,503.80 on the COMEX. Silver hit yet another 31-year high at $46.68 per ounce, with prices ending the week at $46.06. Meanwhile, the U.S. Dollar Index descended to 73.735 during the market day on Thursday, a low unseen since August 2008.2,3

LEI INDEX UP FOR NINTH STRAIGHT MONTH

The Conference Board’s index of leading economic indicators rose another 0.4% for March, complementing a revised 1.0% gain in February. Economists polled by Bloomberg News had forecast a 0.3% advance.4

THIS WEEK: The height of earnings season is upon us. On tap for Monday, we have 1Q results from Netflix and March new home sales data. Tuesday offers earnings reports from Coca-Cola, UPS, 3M, Delta Air Lines, Valero, Ford, Western Union, U.S. Steel, Broadcom and Amazon, along with the February Case-Shiller home price index and the Conference Board’s April consumer confidence index. Wednesday brings 1Q results from eBay, ConocoPhillips, Credit Suisse, General Dynamics, Starbucks, BP, Boeing and Allstate, plus a Fed rate decision and a report on March durable goods orders. Thursday gives us earnings from PepsiCo, P&G, Motorola, Exxon Mobil, Microsoft, Sprint Nextel, Bristol Myers, Viacom and Occidental Petroleum, plus February pending home sales and weekly jobless claims data. What does Friday bring? The March consumer spending report and the University of Michigan’s final March consumer sentiment poll, plus 1Q results from Merck, Caterpillar, Chevron, Weyerhaeuser and DR Horton.

WEEKLY QUOTE

“Don't let what you cannot do interfere with what you can do.”

– John Wooden

WEEKLY TIP

If you’re getting married, inform your partner about all of your debt before the wedding day. Discussing it the day of the wedding or on the honeymoon can kill the mood. Learning about credit and debt issues after the knot is tied can lead to much frustration.

Best Regards,

Kevin Kroskey, CFP, MBA

Citations.

1 - blogs.wsj.com/marketbeat/2011/04/20/existing-home-sales-rise-market-cheers/ [4/20/11]

2 - reuters.com/article/2011/04/21/us-markets-global-idUSTRE71H0EB20110421 [4/21/11]

3 - cnbc.com [4/22/11]

4 - bloomberg.com/news/print/2011-04-21/index-of-leading-economic-indicators-in-the-u-s-rises-0-4-.html [4/21/11]

5 - marketwatch.com/story/sp-cuts-us-rating-outlook-to-negative-2011-04-18 [4/18/11]

6 - cnbc.com/id/42708009 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F22%2F10&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F22%2F10&x=10&y=18 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F22%2F10&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F21%2F06&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F21%2F06&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F21%2F06&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F23%2F01&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F23%2F01&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F23%2F01&x=0&y=0 [4/22/11]

8 - treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield [4/22/11]

9 - treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [4/22/11]

10 - treasurydirect.gov/instit/annceresult/press/preanre/2001/ofm11001.pdf [1/10/01]

11 -montoyaregistry.com/Financial-Market.aspx?financial-market=who-needs-wealth-management-services&category=4 [4/24/11]

This material was prepared by Peter Montoya Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information should not be construed as investment, tax or legal advice. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is an unmanaged, market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is not possible to invest directly in an index. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world's largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

Citations.

1 - blogs.wsj.com/marketbeat/2011/04/20/existing-home-sales-rise-market-cheers/ [4/20/11]

2 - reuters.com/article/2011/04/21/us-markets-global-idUSTRE71H0EB20110421 [4/21/11]

3 - cnbc.com [4/22/11]

4 - bloomberg.com/news/print/2011-04-21/index-of-leading-economic-indicators-in-the-u-s-rises-0-4-.html [4/21/11]

5 - marketwatch.com/story/sp-cuts-us-rating-outlook-to-negative-2011-04-18 [4/18/11]

6 - cnbc.com/id/42708009 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F22%2F10&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F22%2F10&x=10&y=18 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F22%2F10&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F21%2F06&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F21%2F06&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F21%2F06&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=4%2F23%2F01&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=4%2F23%2F01&x=0&y=0 [4/22/11]

7 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=4%2F23%2F01&x=0&y=0 [4/22/11]

8 - treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyield [4/22/11]

9 - treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [4/22/11]

10 - treasurydirect.gov/instit/annceresult/press/preanre/2001/ofm11001.pdf [1/10/01]

11 -montoyaregistry.com/Financial-Market.aspx?financial-market=who-needs-wealth-management-services&category=4 [4/24/11]

This material was prepared by Peter Montoya Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information should not be construed as investment, tax or legal advice. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is an unmanaged, market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is not possible to invest directly in an index. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world's largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.