DOMESTIC ECONOMIC HEALTH Consumers weren’t spending very much, and they weren’t feeling too confident either. Personal spending was flat in May (after ten straight months of gains) and actually decreased 0.1% in inflation-adjusted terms. Both of the major consumer confidence polls went south for June: the Conference Board’s survey dipped 3.2 points to 58.5, and the University of Michigan’s final June consumer sentiment survey retreated to 71.5 from May’s 74.3 mark.2,3,4

Consumer inflation moderated and unemployment increased. The May edition of the Consumer Price Index rose 0.2%; core CPI was up 0.3%. Food prices were up 0.4% and energy prices were up 0.6%, but even so this was the smallest monthly increase in inflation in seven months. Year over year through May, consumer inflation was 3.6% (and core inflation was 1.5%). The Producer Price Index advanced 0.2% in May; the preceding two months had seen increases of 0.7% and 0.8%. Annualized wholesale inflation was 7.3% - the highest wholesale inflation rate since the summer of 2008. The nation’s jobless rate ticked up to 9.1% in May.5,6,7

On the bright side, the Institute for Supply Management’s twin PMI indices signaled that the pace of expansion had accelerated in both the service and manufacturing sectors. ISM’s May service sector index increased 1.8% to 54.6, with a 4.1% boost in new orders. The recently released June manufacturing index was a pleasant surprise: defying expectations of analysts, it rose from 53.5 to 55.3. The Conference Board’s index of leading indicators bounced back from an -0.4& showing in May to go +0.8% in June as eight of ten indicators improved. Durable goods orders had increased by 1.9% during May, and May’s 0.2% dip in retail sales was shallower than analysts had expected.2,8,9,10,11

In Washington, there was much argument over the federal debt ceiling but little agreement. While hiking the debt cap is all but inevitable, Congress elected to take the NFL/NBA approach and sustain the dispute. Meanwhile, Standard & Poor’s warned that it would cut the U.S. debt rating from AAA to D if the debt cap wasn’t raised by August 2; Moody’s threatened a cut to somewhere in its Aa category.12

GLOBAL ECONOMIC HEALTH The International Energy Agency surprised the futures markets in late June when it announced a plan to release 60 million barrels worth of crude from global reserves. In the big picture, the move has a chance to tame inflation pressures (especially in Europe) and aid the dollar.13

Speaking of Europe, reassuring news emerged from the EU as the Greek government embarked on actions to service its debts and stay in the euro. Yet Greece is not out of the woods by any means – the possibility of default still looms, and Standard & Poor’s said it would regard a proposed rollover of privately held Greek debt led by French banks as a “selective default”.14

New manufacturing index data indicated that Asia’s economies were muddling through a soft patch as well. In June, India’s benchmark PMI had its biggest one-month fall since November 2008, reaching a nine-month low of 55.3. Taiwan’s PMI went below 50 for the first time in nine months (meaning sector contraction), and South Korea’s PMI slipped to its lowest level in seven months. China’s official PMI fell to 50.9 for June – a 28-month low.15

WORLD MARKETS Some benchmarks went positive in June, others negative. According to Morningstar calculations in U.S. dollar terms, major Asian benchmarks did okay - Sensex, +2.34%; Nikkei 225, +1.26%; Shanghai Composite, +0.68% (yet Australia’s All Ordinaries went -2.70%). In Europe, the big indices mostly retreated: DAX, +1.11%; CAC 40, -0.62%; FTSE 100, -0.74%; STOXX 600, -2.92%. To our north, Canada’s TSX Composite went -4.41%. The key MSCI indices also lost ground in June (World, -1.73%; Emerging Markets, -1.86%).16,17,18

COMMODITIES MARKETS It was another rough month for the majority of commodities investors. Oil slipped 7.1% in June, a drop aided by the IEA’s surprise call for nations to tap into petroleum reserves. Gold had its second down month in a row (its May-June performance was -3.5%) but remained +5.71% on the year despite a -2.19% month that left prices settling at $1,502.30 on June 30. When the Department of Agriculture said that America had greater inventories and acreage of corn (and other key crops) than estimated, ag futures took a big hit. Wheat lost 21.0%, corn 17.0%, soybeans 6.0% and rice 1.4% in June. Even the dollar lost some ground: the U.S. Dollar Index went -0.21% last month, wrapping up June at 74.54.19,20,21

REAL ESTATE What can you say about a real estate market which features reduced sales activity during the prime homebuying season? There isn’t much positive to report when assessing the May data: existing home sales were down 3.8% while new home sales were down 2.1%. In annual terms, new home sales had improved by 13.5% with the average price better by $1,400;existing home sales were down 15.3% year-over-year with the median price retreating 4.6%.22,23

Speaking of home prices, the April edition of the Case-Shiller/S&P home price index actually showed a 0.7% overall price gain across 20 metro markets – but there was a 4.0% annualized dip in prices to take any celebration out of that small monthly advance. The good news is that pending home sales really rebounded in May: the National Association of Realtors said home sale contracts were up 8.2% from April’s seven-month low and up 17.0% from the June 2010 trough.24,25

Freddie Mac’s June 30 Primary Mortgage Market Survey showed descents in average interest rates on the four common mortgage types compared with its June 2 survey: 30-year FRMs, -0.04% to 4.51%; 15-year FRMs, -0.05% to 3.69%; 5/1-year ARMs, -0.19% to 3.22%; 1-year ARMs, -0.16% to 2.97%.26

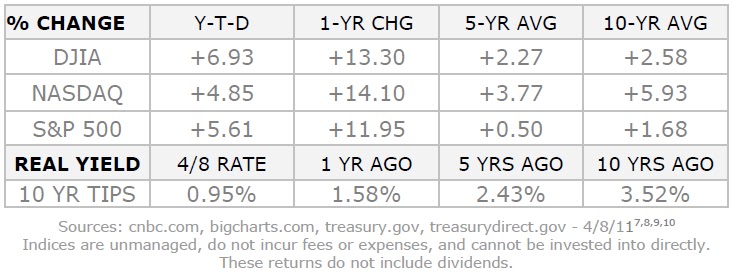

LOOKING BACK…LOOKING FORWARD Early in June, bears were groaning. By the end of the month, the bulls were back in charge. In fact, June 27-July 1 represented the best week for the Dow and S&P 500 since mid-July 2010. Still, it was a negative month for stocks.27

So with this newfound momentum or at least interest in equities, we find ourselves in July – traditionally a pretty good month on Wall Street, powered by anticipation of 2Q earnings. Since 2000, July has been a little less positive than in previous stock market cycles: the Stock Trader’s Almanac notes that the Dow and S&P have respectively averaged July gains of 1.24% and 0.16% in the last 11 years, with the NASDAQ averaging a 0.45% loss for the month. That is the recent history. The current reality is that we still have concerns about a flagging world economy, severe debt problems plaguing multiple EU countries and no agreement yet on the federal debt ceiling. Let’s hope that earnings season casts its spell on the collective mind of Wall Street, with 2Q results impressive enough to make stock market performance in July 2011 correspond to Julys of decades before.32

UPCOMING ECONOMIC RELEASES: Looking at the balance of July, here is what’s ahead: the June ISM service sector index (7/6), the June jobs report and May wholesale inventories (7/8), June PPI and retail sales and May business inventories (7/14), June CPI and industrial output and the initial University of Michigan July consumer sentiment survey (7/15), June building permits and housing starts (7/19), June existing home sales (7/20), the Conference Board’s LEI index for June (7/21), June new home sales, May’s Case-Shiller home price index and the Conference Board’s July consumer confidence poll (7/26), June durable goods orders and a new Federal Reserve Beige Book (7/27), June pending home sales (7/28), and the first take on 2Q 2011 GDP and a final June consumer sentiment poll from the University of Michigan (7/29). The Commerce Department report on June consumer spending will be released on August 2.

MONTHLY QUOTE

“The large print giveth, but the small print taketh away.”

– Tom Waits

– Tom Waits

MONTHLY TIP

How big is your rainy day fund? Ideally, you should build an emergency fund that should equal 6-12 months of current living expenses. It is a worthwhile goal to pursue.

Best Regards,

Kevin Kroskey

Citations.

1 - blogs.wsj.com/marketbeat/2011/06/30/data-points-u-s-markets-27/ [6/30/11]

2 - cnbc.com/id/43546166/ [6/27/11]

3 - blogs.wsj.com/marketbeat/2011/07/01/ism-much-better-than-expected/ [7/1/11]

4 - marketwatch.com/story/consumer-sentiment-declines-in-june-2011-07-01 [7/1/11]

5 - bls.gov/news.release/cpi.nr0.htm [6/15/11]

6 - bls.gov/news.release/ppi.nr0.htm [6/14/11]

7 - latimes.com/business/la-fi-jobs-report-20110604,0,3594048.story [6/3/11]

8 - ism.ws/ISMReport/NonMfgROB.cfm [6/3/11]

9 - bloomberg.com/news/2011-06-17/u-s-leading-economic-indicators-index-rises.html [6/17/11]

10 - marketwatch.com/story/us-durable-goods-orders-rise-19-for-may-2011-06-24 [6/24/11]

11 - marketwatch.com/story/retail-sales-fall-for-first-time-in-11-months-2011-06-14-919560 [6/17/11]

12 - bloomberg.com/news/2011-06-29/moody-s-would-likely-cut-u-s-debt-rating-to-aa-range-in-event-of-default.html [6/30/11]

13 - online.wsj.com/article/BT-CO-20110627-712832.html [6/27/11]

14 - investors.com/NewsAndAnalysis/Article/577212/201107050905/Stock-Futures-Nose-Lower-Baidu-Adds-2.htm [7/5/11]

15- reuters.com/article/2011/07/01/economy-global-pmi-idUSL3E7I10O820110701 [7/1/11]

16 - news.morningstar.com/index/indexReturn.html [6/30/11]

17 - mscibarra.com/products/indices/international_equity_indices/gimi/stdindex/performance.html [6/30/11]

18 - blogs.wsj.com/marketbeat/2011/06/30/data-points-europe-135/ [6/30/11]

19 - blogs.wsj.com/marketbeat/2011/06/30/data-points-energy-metals-494/ [6/30/11]

20 – online.wsj.com/mdc/public/npage/2_3051.html?mod=mdc_curr_dtabnk&symb=DXY [7/5/11]

21 - businessweek.com/news/2011-07-01/corn-extends-worst-monthly-loss-since-2008-on-acreage-increase.html [7/1/11]

22 - money.cnn.com/2011/06/23/real_estate/new_home_sales/?section=money_latest [6/23/11]

23 - nytimes.com/2011/06/22/business/economy/22econ.html [6/22/11]

24 - blogs.forbes.com/morganbrennan/2011/06/29/what-can-homeowners-learn-from-case-shillers-home-price-index/ [6/29/11]

25 - usatoday.com/money/economy/housing/2011-06-29-pending-home-sales_n.htm [6/29/11]

26 - freddiemac.com/pmms/ [7/5/11]

27 - cnbc.com/id/43608555 [7/1/11]

28 - bigcharts.marketwatch.com/historical/default.asp?symb=DJIA&closeDate=6%2F30%2F10&x=0&y=0 [7/5/11]

28 - bigcharts.marketwatch.com/historical/default.asp?symb=COMP&closeDate=6%2F30%2F10&x=10&y=18 [7/5/11]

28 - bigcharts.marketwatch.com/historical/default.asp?symb=SPX&closeDate=6%2F30%2F10&x=0&y=0 [7/5/11]

29 - treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldYear&year=2011 [7/5/11]

30 - treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspx?data=realyieldAll [7/5/11]

31 - treasurydirect.gov/instit/annceresult/press/preanre/2001/ofm11001.pdf [1/10/01]

32 - cnbc.com/id/43197003 [5/31/11]

33 - montoyaregistry.com/Financial-Market.aspx?financial-market=financial-planning-where-do-you-begin&category=5 [7/6/11]

This material was prepared by MarketingLibrary.Net Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is an unmanaged, market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is not possible to invest directly in an index. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world's largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. BSE Sensex or Bombay Stock Exchange Sensitivity Index is a value-weighted index composed of 30 stocks that started January 1, 1986. Nikkei 225 (Ticker: ^N225) is a stock market index for the Tokyo Stock Exchange (TSE). The Nikkei average is the most watched index of Asian stocks. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The S&P/ASX All Ordinaries Index represents the 500 largest companies in the Australian equities market. The DAX 30 is a Blue Chip stock market index consisting of the 30 major German companies trading on the Frankfurt Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSE 100 Index is a share index of the 100 most highly capitalized companies listed on the London Stock Exchange. With a fixed number of 600 components, the STOXX Europe 600 Index represents large, mid and small capitalization companies across 18 countries of the European region. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The MSCI World Index is a free-float weighted equity index that includes developed world markets, and does not include emerging markets. The MSCI Emerging Markets Index is a float-adjusted market capitalization index consisting of indices in more than 25 emerging economies. The US Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability and differences in accounting standards. All information is believed to be from reliable sources; however we make no representation as to its completeness or accuracy. All economic and performance data is historical and not indicative of future results. Market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.