The stock market seems to be climbing the proverbial "wall of worry."

Despite potential road hazards such as sovereign debt issues, rising interest rates, a weak job market, and a stalled housing recovery, investors bid up stock prices last week to an 18-month high, according to MarketWatch. Of course, these things could eventually affect stock prices, but, for now, stocks are riding the momentum of improving earnings and some underlying stability in the economy.

Lack of job growth has been a major problem for our economy the past couple years, but that could change this week. On April 2, the government will release the March employment report and, according to CNBC, economists expect it to show a rise of about 200,000 non-farm jobs. That would be a small down payment on the 8.4 million jobs lost since December 2007, according to Bloomberg. The fact that the S&P 500 has risen for four consecutive weeks may suggest that the market has been anticipating a good report. Ironically, on the day the employment report is released, the U.S. stock market will be closed for the Good Friday holiday, so we won't know the market's reaction until the following Monday.

Fear of a double-dip recession seems to be fading, too. In its final revision, the Commerce Department said fourth quarter 2009 GDP increased at a 5.6% annualized rate, which is the fastest rate in six years. For 2010, economists surveyed by MarketWatch expect GDP to expand at a non-recessionary 3% rate. On a regional note, the Great Lakes commercial shipping season has started early partly due to increased demand for iron ore and coal. "Things are moving quicker, sooner than a year ago. And it seems like more ships are involved," said Eric Reinelt, Port of Milwaukee executive director as quoted in the March 28 edition of the Milwaukee Journal Sentinel.

So, despite the worries, there is some good economic news supporting stock prices.

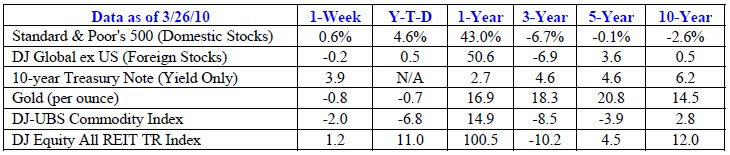

Notes: S&;P 500, DJ Global ex US, Gold, DJ-UBS Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; the DJ Equity All REIT TR Index does include reinvested dividends and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods.

Sources: Yahoo! Finance, Barron’s, djindexes.com, London Bullion Market Association.

Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable or not available.

THE DAY OF RECKONING due to our country's ballooning deficits may be getting closer. Back in 2008, the Congressional Budget Office (CBO), projected the U.S. would run a budget surplus of $247 billion for the years 2009 through 2018. Now, just two years later, CNBC and the CBO have crunched the numbers again and project that we will incur a $7.4 trillion deficit during that 10-year period, according to a March 26 CNBC article.

How could the situation deteriorate so much in just two years?

The CBO said 57% of the projected deficit increase was due to lower government revenues--much of which is due to the decline in our economy and projected sluggish economic growth. The other 43% included expenses such as, "the stimulus bill, a change in accounting for the war, extended unemployment benefits, and additional interest on debt."

At the end of 2009, the U.S. national debt stood at $12.3 trillion, according to the Treasury Department. Tack on the projected deficit over the next 10 years and we could be close to $20 trillion in the hole 10 years hence.

Like chocolate chip cookie dough, a spoonful of annual deficit and national debt is fine, but gorging our country on borrowed money may eventually cause significant problems. Too much government debt could lead to rising interest rates and slower economic growth, according to Fortune Magazine. In a worst-case scenario, it could lead to economic collapse.

We have several options to solve the budding debt problem before it gets completely out of hand. First, we could grow our way out of it. This is the preferred method and the least painful. Second, we could raise taxes. Third, we could cut government spending. Most likely, we'll see a combination of the three.

Given the magnitude of our swelling deficits, we will likely have pain in our future. Whether that pain happens in our generation, our children's, or our grandchildren's, remains to be seen.

Weekly Focus – Think About It

"The way to wealth depends on just two words, industry and frugality."

--Benjamin Franklin

Best regards,

Kevin Kroskey

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this e-mail with their e-mail address and we will ask for their permission to be added.

* This newsletter was prepared by PEAK.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general.

* The DJ Global ex US is an unmanaged group of non-U.S. securities designed to reflect the performance of the global equity securities that have readily available prices.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Gold represents the London afternoon gold price fix as reported by the London Bullion Market Association.

* The DJ Commodity Index is designed to be a highly liquid and diversified benchmark for the commodity futures market. The Index is composed of futures contracts on 19 physical commodities and was launched on July 14, 1998.

* The DJ Equity All REIT TR Index measures the total return performance of the equity subcategory of the Real Estate Investment Trust (REIT) industry as calculated by Dow Jones.

* Yahoo! Finance is the source for any reference to the performance of an index between two specific periods.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Past performance does not guarantee future results.

* You cannot invest directly in an index.

* Consult your financial professional before making any investment decision.