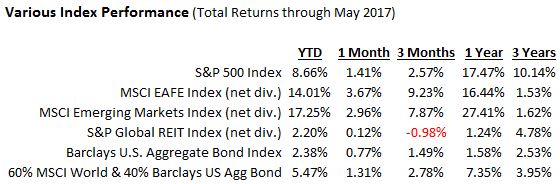

After gaining 3.07% for November, the S&P 500 has now posted its eighth consecutive month of positive returns. International markets were up more modestly recently while bond returns were negative at -0.13% in November. For 2017, a 60% global stock and 40% bond portfolio is now up more than 13%; 40% global stock portfolio nearly 10%.

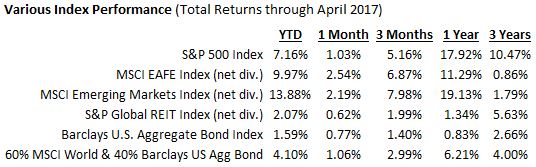

| Index | YTD | 1 Mo. | 3 Mo. | 3 Years | 5 Years |

| S&P 500 Index | 20.49% | 3.07% | 7.65% | 10.91% | 15.74% |

| MSCI EAFE Index (net div.) | 23.06% | 1.05% | 5.14% | 5.97% | 8.24% |

| MSCI Emerging Markets Index (net div.) | 32.53% | 0.20% | 3.30% | 6.15% | 4.61% |

| S&P Global REIT Index (net div.) | 6.32% | 3.01% | 1.51% | 4.08% | 7.32% |

| Barclays U.S. Aggregate Bond Index | 3.07% | -0.13% | -0.55% | 2.11% | 1.98% |

| 100% MSCI All Country World Index (net div.) | 22.01% | 1.94% | 6.06% | 8.01% | 10.94% |

| 60% MSCI World & 40% Barclays US Agg Bond | 13.39% | 1.25% | 3.60% | 5.87% | 7.88% |

| 40% MSCI World & 60% Barclays US Agg Bond | 9.86% | 0.79% | 2.21% | 4.66% | 5.92% |

Key Economic News

- Employment: Total employment rose by 261,000 in October following September's job reduction. The unemployment rate edged down to 4.1%. Over the 12 months ended in October, average hourly earnings have risen $0.63, or 2.4%.

- Interest rates: The Federal Open Market Committee met at the end of October and left the target federal funds rate range at 1.00%-1.25%. However, some economic indicators are showing mild inflationary pressures, which, when coupled with a labor market that could be nearing full employment, may lead to another interest rate hike when the Committee next meets in mid-December.

- GDP: The second estimate of the third-quarter gross domestic product showed expansion at an annual rate of 3.3%, according to the Bureau of Economic Analysis. The second-quarter GDP grew at an annualized rate of 3.1%.

- Inflation: For the 12 months ended in October, consumer prices (CPI) are up 2.0%, a mark that approaches the Fed's 2.0% target for inflation. Core prices, which exclude food and energy, increased 0.2% in October, and are up 1.8% over the prior 12 months.

Looking Ahead

All indications are that the Federal Reserve will relax stimulus measures by increasing the federal funds interest rate when the Committee meets this month.

As always: stay disciplined and focus on those things you can control.

To Your Prosperity,

Kevin Kroskey, CFP®, MBA

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e. wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.